As retirement gets closer, your Social Security statement becomes more than just a benefits estimate. It can help inform decisions around retirement timing, income planning, taxes, Medicare costs, and portfolio withdrawals.

For high-income earners and retirees with multiple income sources, Social Security is often less about replacing income and more about coordinating benefits within a broader retirement strategy. Yet many people reviewing their statement for the first time are surprised by what it includes—and what it leaves out.

This guide walks through how to read your Social Security statement, what the numbers mean, and several important considerations not reflected in the estimate itself.

You can access your Social Security statement online through the Social Security Administration’s “my Social Security” portal.

1. Visit the Social Security Administration website

2. Create a “my Social Security” account (if you do not already have one)

3. Access your earnings history and estimated retirement benefits

If you do not create an online account, the Social Security Administration generally mails statements to individuals beginning around age 60.

Even for households with substantial retirement assets, understanding your estimated Social Security benefits can inform broader decisions about retirement income, taxes, and timing.

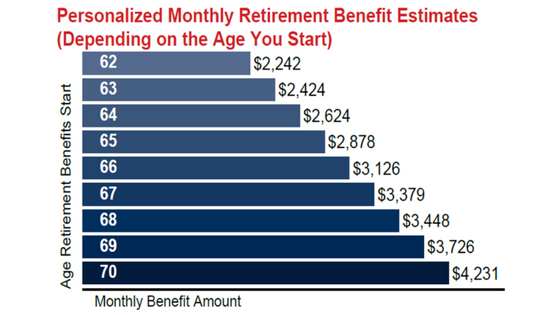

One of the first things most people notice is the estimated benefits graph.

The graph estimates your future monthly retirement benefit based on your current earnings history and projected future earnings.

For example, someone currently earning at or above the Social Security wage base may see projected benefits assuming they continue earning a similar income until retirement.

One important takeaway from the statement is that benefits can vary depending on when you choose to begin taking them.

One of the most important Social Security decisions is not just what your benefit is, but when you choose to claim it.

For individuals born after 1960, full retirement age is generally 67. However, benefits can begin earlier or later, depending on your situation and preferences.

You can begin taking Social Security retirement benefits as early as age 62, but doing so permanently reduces your monthly benefit.

Benefits are reduced:

For someone with a full retirement age of 67 who claims at age 62, the reduction can be as much as 30%.

For some retirees, claiming early may provide additional flexibility or income sooner. For others, waiting may better align with long-term retirement income goals.

Waiting until full retirement age (FRA) allows you to receive your full calculated retirement benefit based on your earnings history.

For many households, this is a middle-ground approach between taking benefits early and delaying them for additional growth.

For each year you delay benefits beyond full retirement age, your benefit increases by about 8% annually until age 70.

For example, someone whose full retirement age is 67 could substantially increase their monthly benefit by waiting until age 70 to begin receiving benefits.

Related article: The Pros and Cons of Filing for Social Security Before Full Retirement Age

One critical takeaway from the graph above is the growth of the benefits over time. For those born after 1960, the full retirement age for Social Security is 67. But you can elect to take benefits sooner or delay benefits. Here's what it could mean for you:

| Claiming Decision | What Happens | Trade-Off |

| Claim at 62 | Lower monthly benefit | Receive income sooner, but with permanently reduced benefits |

| Claim at 67 | Full retirement benefit | Balanced approach for many retirees |

| Claim at 70 | Benefit increases approximately 8% annually until 70 | High future income, but requires delaying withdrawals |

While the Social Security statement provides useful estimates, it omits several key retirement planning considerations.

Your statement does not include Medicare Part B premiums, which are typically deducted directly from Social Security benefits after enrollment.

Because Medicare premiums can change annually, it is important to review current premium levels when estimating retirement income.

The statement also does not reflect Income-Related Monthly Adjustment Amounts (IRMAA), which can increase Medicare premiums for higher-income retirees.

For affluent households, this can be an important coordination point among:

The statement may also omit:

These rules can affect individuals who receive pensions from employment not covered by Social Security taxes.

If you worked in certain government or public-sector roles, additional review may be warranted.

For higher earners, Social Security often plays a different role in retirement planning, not necessarily as the primary income source, but as one piece of a broader income strategy.

Social Security includes an annual wage base, meaning earnings above a certain threshold are not subject to Social Security tax.

As a result:

This is one reason why Social Security timing decisions are often coordinated alongside:

If you are unsure whether your earnings exceeded the Social Security wage base over time, your taxed earnings history can be found on page two of your Social Security statement.

Related article: Are Social Security Benefits Worth More Than You Think?

The Social Security Administration recommends periodically reviewing your statement to confirm:

Even small inaccuracies in your earnings record could affect future benefit calculations.

If you discover missing or incorrect earnings:

Gather documentation supporting the correction

Contact the Social Security Administration directly

Social Security decisions rarely occur in isolation.

As retirement approaches, benefit timing decisions may intersect with:

For many households, the goal is not simply to maximize Social Security benefits, but to understand how Social Security fits within the broader retirement picture.

Your estimate assumes you continue earning at a similar income level until retirement. Actual future earnings and retirement timing can affect final benefits.

The appropriate timing depends on factors such as longevity expectations, retirement income needs, taxes, and overall financial circumstances.

No. Medicare premiums and IRMAA surcharges are not reflected in your Social Security benefit estimate.

Only up to a limit. Earnings above the Social Security wage base are not taxed for Social Security purposes and generally do not increase future benefits.

Gather supporting documentation and contact the Social Security Administration to request corrections.

Your Social Security statement can provide valuable insights for retirement planning, but it is only one piece of the picture.

As retirement gets closer, understanding how Social Security interacts with taxes, Medicare, portfolio withdrawals, and other income sources may become increasingly important.

As retirement approaches, decisions about Social Security often intersect with taxes, investment withdrawals, Medicare costs, and long-term income planning.

If you would like help understanding how these pieces fit together for your situation, we’re happy to start a conversation.

Any discussion of taxes is for general information purposes only, does not purport to be complete or cover every situation, and should not be construed as legal, tax, or accounting advice. Clients should confer with their qualified legal, tax, and accounting advisors as appropriate.

CRN202905-11154212

Jordan Bilodeau, CFP®, is a Partner and the Director of Planning & Strategy at Spaugh Dameron Tenny, where he leads firmwide planning initiatives and helps clients navigate complex financial decisions. With experience in portfolio design, tax strategies, and business succession planning, Jordan works with executives, physicians, dentists, and successful retirees to coordinate every aspect of their financial lives. He holds the CERTIFIED FINANCIAL PLANNER® designation and has a Master’s degree in Wealth and Trust Management, providing tailored guidance for clients.

/Logo%20Horizontal%20(4).png?width=2000&name=Logo%20Horizontal%20(4).png)