The unpaid time between training and practice is probably the one area of planning that catches most residents and fellows off guard. Transition planning involves preparing for the financial and lifestyle changes that take place as you transition from training to practice.

This is a time period when a lot of new decisions need to be made, such as:

How can you set yourself up for transition success? Let’s explore the questions you should ask before the transition and how much you should budget during this period.

With entering into new transition territory, you may have a few things that you need to get clarity on beforehand. Here are a few of the questions you should ask yourself before transitioning:

The answer to this is typically yes. Other questions you should ask yourself should include: what will you do to insure yourself and your family during that time? When will your new health insurance start? Should you consider your employer’s COBRA options or an alternative solution?

NOTE: It is very important to know COBRA start and end dates and confirm them, as well as the start date for your new employer’s health insurance.

The bottom line is that all of these considerations require cash. Without planning for your transition period, the default could be to run up credit card debt or take out a loan. Sometimes, this is the only option.

If, for example, this is the first time you’ve considered saving for your transition period and it’s coming up in a month, it’s probably not possible for you to save up enough cash to last through that time without using your credit card. If this is the case, you want to make sure part of your new budget accounts for paying off your credit card debt and establishing an emergency fund as soon as possible.

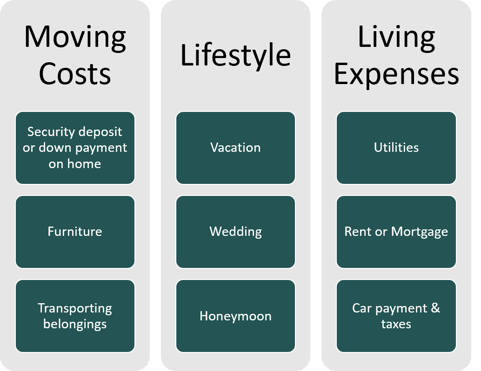

The transition period is also typically a time when many physicians get married, move, or take vacations. Your buffer of savings may be needed to cover some or all of the following expenses:

It's important to note that moving costs are sometimes reimbursed, but typically you must initially pay out-of-pocket. The list of expenses above does not include miscellaneous daily costs of living while in transition.

Based on our experience, we’ve worked with physicians who may need anywhere from $5,000 - $40,000 for a comfortable transition. Why does this number vary so much? It all depends on the external factors. Let’s dive-in.

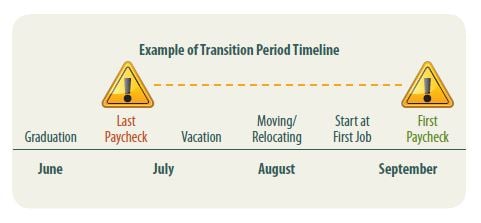

Transition period timeline:

Typical Transition Period Scenario: Congratulations! You have just taken a job at a private practice in Charleston. Your new position starts August 1. You finish training on June 20, and have enough savings to stay afloat for the end of June and the month of July. Unfortunately, your new practice pays monthly, and so you won’t receive your first paycheck until September 1. Now you are left using your credit card or borrowing money from your family until you get paid, even though you’ve already begun working. The earlier you can start planning for your transition period, the less negative impact it will have on your financial health.

While you may not know exactly what your transition period will look like ahead of time, you can do your best to prepare for this change. By having a plan in place, you can make sure you are ready for the time between training and your new career so that you are not left without financial stability in this uncertain transitional period.

If you are still at a loss for what to do financially in your transition journey, download the fellowship financial guide to give you additional clarity through the process. This guide help you understand the importance of creating a financial plan, uncover how you are managing your budget currently, find out your net worth, and more!

CRN202202-260583

John Dameron has been a financial planner and partner with Spaugh Dameron Tenny since 2002. With the help of the SDT team, John created a lecture series called Physicians Financial Focus, authored a book entitled The Residents and Fellows Financial Survival Guide, and has coached hundreds of physicians from residency/fellowship into practice. His expertise has also been featured on KevinMD.

/Logo%20Horizontal%20(4).png?width=2000&name=Logo%20Horizontal%20(4).png)